Zhejiang Hengtong's Strategic Waiver: Opportunity or Prudence?

In a significant corporate decision, Zhejiang Hengtong Holdings recently announced its waiver of the right to acquire 51% of Hebei Shengxue Dacheng Pharmaceutical Co., Ltd. from China Nuclear Uranium Industry Co., Ltd. for approximately 556.6 million yen. This move, while seemingly inconsequential at first glance, reflects a delicate balance in the company’s strategic approach towards its investment landscape, particularly amid a backdrop of fluctuating market dynamics and growing investment risks in the pharmaceutical sector.

The consensus among Hengtong's board of directors to unanimously approve this waiver underscores internal alignment and a considered approach toward stakeholder management. Holding onto a 49% stake in Shengxue Dacheng, however, may prompt questions about their potential influence over future operational strategies—as the pharmaceutical industry is increasingly defined by partnerships and collaborations that can drive innovation and profitability. If Shengxue Dacheng performs well post-transfer, Hengtong could find itself on the sidelines of future growth opportunities, raising the critical question: Did Hengtong sufficiently evaluate the potential return on investment in waiving these rights?

From a financial standpoint, the latest figures reveal a complex picture despite the seemingly stable metrics. Hebei Shengxue Dacheng's total assets have shown slight growth, which is commendable, yet the reduction in liabilities suggests a more robust financial resilience. However, accompanied by a notable drop in net profit from 5.91 billion yen in 2024 to only 2.46 billion yen in the initial months of 2025, a troubling narrative emerges regarding operational efficiency. This decline in profitability, juxtaposed with improvements in liabilities and equity, indicates potential misalignment between asset management and revenue generation. Investors may be questioning whether Hengtong's current trajectory is sustainable or artificially inflated by favorable asset positions.

Moreover, monitoring external variables—such as the financial health of potential stakeholders like China Nuclear Uranium and its implications for Shengxue Dacheng—is paramount. Failure in this regard could destabilize not just the operational paradigm of Shengxue Dacheng but also Hengtong’s strategic planning overall. The exclusion of some assets from consolidation raises another important risk aspect, as dependency on select assets may amplify vulnerabilities should market conditions evolve unfavorably. Therefore, there is an undeniable call for vigilance from institutional investors amid these shifting undercurrents.

In conclusion, while Zhejiang Hengtong Holdings may not face immediate repercussions from waiving its equity rights in Shengxue Dacheng, the broader implications warrant careful scrutiny. The interplay between operational efficiencies, strategic decision-making, and market conditions reflects an environment rife with opportunity yet equally laden with potential pitfalls. Investors looking to navigate this evolving landscape should consider both the current strengths and the fragility suggested by declining profitability metrics. As market dynamics continue to shift, will Hengtong seize future opportunities, or will this decision echo as a missed milestone in its growth trajectory?

Read These Next

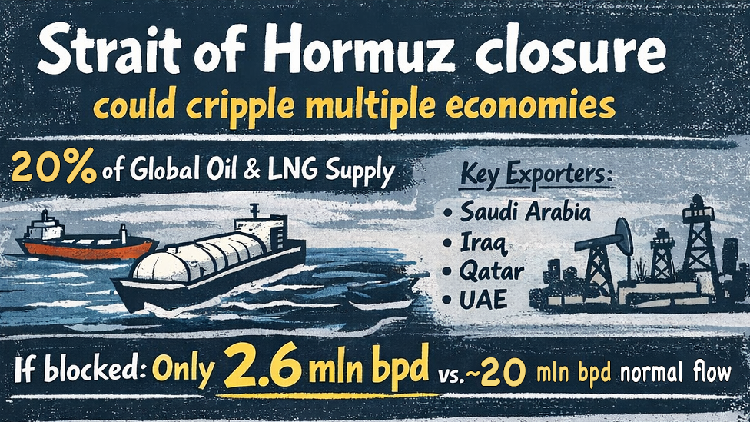

Strait of Hormuz Closure Threatens Global Economies

Closure of the Strait of Hormuz could disrupt global oil supply and economies, highlighting the need for diplomatic engagement.

Deep Tianma Repurchases 184391 Million Shares for 173 Million Yuan

Shenzhen Tianma A repurchased 18.4M shares for 173M yuan by Feb 2026, boosting shareholder returns and investor confidence.

Capital Management in Hong Kong: Recent Developments Overview

This commentary provides a critical analysis of recent changes in a Hong Kong-based company's capital and stock options, with a focus on market compliance, risk factors, and financial trends.